Market Update Q1 2026

11th February 2026

Market snapshot: Q1 2026

Diverging performance driven by supportive fundamentals

Markets remain supported by solid earnings, with strength in AI-linked technology, defence, and infrastructure. Returns are becoming more uneven as interest rates remain higher than in the post‑GFC era, despite recent cuts, with geopolitical developments further widening differences across regions and sectors. US politics continues to influence markets, particularly where decisions impact interest rate and inflation expectations.

Movements relative to previous quarterly update.

* Returns above are calculated from the GBP total return index of each index, for respective dates between 01/01/2025 and 31/12/2025; ¹ previously reported reverse repo rate. Replaced with one-year Loan Prime Rate (LPR) for this and future reports; ² previously deflation – shift to inflation a positive move for the economy.

Macroeconomic outlook: momentum has slowed, growth remains positive

Limited signs of strong economic acceleration, growth likely to be uneven across regions and sectors

- Interest rates: the Fed cut twice in Q4 and the Bank of England once, while the ECB and PBoC held steady. Markets expect no further US moves before the May Chair transition despite political pressure. UK markets still price more easing. Earlier fears that politically driven US cuts could force the UK and EU into tighter policy to control inflation have largely abated with the nomination of a Fed Chair known for taking a tougher line on inflation.

- Inflation: US inflation and expectations improved, though risks remain, with tariff threats and if interest rates are cut too quickly. UK inflation is sticky but is forecast to keep declining, helped by weakening wage growth. EU inflation is on target, with a stable outlook. China’s deflation appears to have turned around, with prices rising in each month of the quarter.

- Employment: US jobs appeared firm, but annual growth was the weakest in two decades outside major recessions and labour ’s share of GDP hit a record low. The UK saw the fastest job cuts since 2020 and slowing wage growth. EU and China unemployment improved, but slow economic growth is still a risk.

Central Banks: Fed – the United States Federal Reserve; BoE – Bank of England; ECB – European Central Bank; PBoC – People’s Bank of China

UK markets – “the year the country turns a corner” Rachel Reeves (Chancellor of the Exchequer)

UK markets performed strongly in 2025, led by cash‑generating sectors such as telecoms, financials, industrials, and basic materials. AI gains were concentrated in infrastructure and utilities rather than high‑growth software like in the US. Sterling held steady and growth expectations improved, though business confidence weakened on tax and regulatory concerns. Even so, firms expect better domestic and export demand, and the market continues to favour value, stability, and income over high‑risk growth. Epstein revelations may impact country leadership.

Outlook – Truth, Trust, and Trade – a new power-based order?

- US volatility still sets global tone: a dramatic beginning to the year underscored how tightly global markets still track US volatility. Threats of force, tariff moves, and pressure on Fed independence all swung sentiment. The World Economic Forum in Davos also signalled a shift, highlighting a move by middle powers to coordinate and diversify trade away from the US. The Supreme Court is yet to rule on the legality of Trump’s 2025 tariffs under the banner of an ‘economic emergency’.

- Fiscal cracks: Japan’s bond wobble a warning for the US: the Japanese government’s food‑tax announcement revived fears over its 250% debt load and sparked an unusual jump in long‑term yields. The successful re-election of Sanae Takaichi has settled bond markets somewhat, but there is still uncertainty around funding her party’s fiscal policies. The reaction offers a caution for the US, where persistent deficits and political dysfunction could prompt investors to reprice dollar risk.

- Global reserve under scrutiny: gold surged past $5,000/oz in January, up 51.3% in 2025 and beating every major market. Growing debate over US debt, political volatility, and the dollar ’s reserve role is making precious metals attractive as a diversifying store of value. We discuss silver as a topic this quarter. Trump’s unexpected nomination of a hawkish Fed Chair (Kevin Warsh) – one likely to prioritise controlling inflation over cutting interest rates – surprised world markets, sending gold and silver prices lower and boosting the US dollar. Overall, the market is positive with Trump’s nomination of Kevin Warsh, but the battles are not over to ensure independence of the Fed.

Short term outlook: up to 1 year

US

- The “maturity wall” of US debt rollover takes place over 2026; the incremental cost of increased borrowing costs is likely to be in the region of $130bln – $200bln per year, knocking between 0.4% – 0.7% off US GDP.

- Supreme Court ruling on legality of tariffs is imminent, markets give a 70% chance the Supreme Court will rule against Trump.

- Trump has withdrawn threats of military action to take Greenland and to impose tariffs on the EU. However market odds give a 12% chance Trump will make another bid for Greenland before the end of the year.

- New Fed chair, Warsh, will be caught in a Senate battle to withdraw charges against outgoing chair Powell.

- Ongoing US govt shutdowns driven by deadlock over funding bills, including homeland security, exacerbated by tensions over ICE agent fatal shootings. This is likely to negatively impact the dollar and potentially support gold demand.

- Economists anticipate that the mid‑terms will temper Trump’s erratic policies at the end of the Summer.

Japan

- Sanae Takaichi’s Liberal Democratic Party (LDP) secured a majority in the Lower House in the February 8 election. Economists are concerned that Japan’s populist, debt‑fuelled spending plans will weaken the yen and raise inflation.

- Bank of Japan governor noted in late January that “addressing rising prices is an urgent priority in Japan, the bank should not take too much time examining the impact of raising the policy interest rate, and should proceed with the next step, a rate hike, without missing the appropriate timing.”

China

- Emerging with India as a flag bearing deal partner for the ‘middle powers’

- In April Trump is expected to work to persuade Chinese Premier, Xi, to carve up the world according to US‑China interests.

Europe

- Will work to re‑arm and build European defence and intelligence capability without the US.

Medium term outlook: 1 – 3 years

Energy concerns from AI continue, productivity increases likely across the globe.

Conflict regions

- Russia: around 93 sanctioned tankers continue to support illegal fuel trade.

- Israel: ongoing hostilities with militant groups and complex diplomacy.

- Iran: odds of regime change have softened, no credible alternative to Khamenei or military dictatorship power at time of writing.

- Somalia/Yemen: conflicts likely to be destabilising to oil tanker traffic.

- Broader Asia: likely to continue to develop into new global powers.

Primer: The rise and (potential) fall of dollar credibility

Post WWII and Bretton Woods: USD becomes anchor, Fed gains global responsibility

Allied nations sought to rebuild the global economy and avoid another depression. Bretton Woods established the USD as the system’s anchor, backed by America’s vast gold reserves (two‑thirds of known reserves) and trust in the US, which was high post‑war. Countries maintained stable exchange rates against the dollar, often using capital controls. The IMF and World Bank were created. This framework kept inflation artificially low.

1971 – Nixon Shock: end of gold convertibility and collapse of Bretton Woods

Heavy US spending on Vietnam and social programs led to more dollars being issued than gold held. Foreign governments demanded gold, draining reserves. Nixon ended gold convertibility, major currencies floated, and inflation surged as money creation was no longer constrained.

With gold constraints gone, central banks kept rates low and governments spent freely, driving demand‑side inflation.

1970s Great Inflation and petrodollars

Demand driven inflation collided with supply shocks from the oil embargo (1973‑4) and Iranian Revolution (1979‑80). A US‑Saudi deal priced global oil in USD, creating “petrodollars’ – oil revenues which flowed into US Treasuries, lowering US borrowing costs. The US dollar is still the dominant currency for settling oil contracts however oil producing countries are now seeking diversification.

Hard money ‘revolution’

Major inflation in the 1970’s led central banks to move toward modern monetary policy, underpinned by ‘hard‑money’ principles: Inflation must be prevented, control money supply growth, actively increase interest rates when inflation rises, maintain independence from political pressure, and keep price stability.

1979‑80: Paul Volcker (Fed Chair) raised interest rates to nearly 20%, crushing inflation, but triggering a deep recession. Whilst painful domestically, it restored credibility in the value of the USD and the Fed’s commitment to controlling inflation – the anchor of modern monetary policy, and central to current debates around the role and independence of the Fed.

Divergent Models: PBOC vs BoJ

The People’s Bank of China (PBOC) remains state‑directed, tightly managing the exchange rate, controlling capital flows, and holding large USD reserves—closer to a Bretton Woods‑style regime than an inflation‑targeting one. Notably the PBOC has actively bought US assets to balance trade surpluses.

2008 Global Financial Crisis to today

Quantitative Easing became a policy tool and the world synchronised with the US in credit, asset price, and capital flow cycles with the US. The Federal Reserve has expanded from a domestic stabiliser into a de facto global lender of last resort, supplying dollar liquidity to major central banks through standing and emergency swap lines. Japan already has access to these facilities via the Bank of Japan, but any activation would be closely watched by markets as a signal of global dollar funding stress rather than sovereign distress.

US dollar (USD) as global reserve currency

Long‑standing trust in US institutions, rule of law, and geopolitical power underpins confidence.

The USD is the dominant global trade, funding, and reserve currency, and widespread dollar use is self‑reinforcing, making replacement difficult.

The Trump administration impact on the dollar

Since President Trump returned to office in January 2025, the US dollar has broadly weakened against a basket of major currencies: the US Dollar Index (DXY) – a standard measure of the greenback’s value – is down roughly 8 – 11% from early 2025 levels, marking one of the steepest annual declines in decades as trade‑policy uncertainty, tariff shocks, fiscal concerns, and expectations of politically motivated Federal Reserve rate cuts have weighed on the currency. While Venezuela had been pricing oil outside the dollar, in Chinese Yuan, there is no hard evidence that Nicolás Maduro was captured specifically to stop a shift toward yuan-priced oil, even if U.S. concerns about dollar primacy formed part of the broader geopolitical backdrop.

Reserve assets and the dollar system: who holds the power?

Foreign Holdings of US Reserves, 2025

Treasury holdings are not easy to manipulate: a country dumping US dollars would self-inflict losses by depressing prices and raising yields, so real leverage comes from marginal diversification away from Treasuries and the dollar.

Risks to USD as Global Reserve Currency

- Fiscal position and trajectory: US rising debt and deficits affect confidence.

- Political instability: US governance risks are increasing and there is a lack of united front on debt‑ceiling.

- Loss of institutional credibility: e.g. Growing perceptions of politically influenced legal decisions weaken the rule of law; if Fed independence erodes, the anchor for inflation expectations weakens, raising the risk of a broader loss of policy credibility.

Observed Shifts Out of US Treasuries

- There is evidence some investors now view Treasuries as more of a risk asset, rather than a default safe haven. Recent muted flight‑to‑quality suggests investors are reassessing the “safe asset” story.

- European fund managers say their move out of Treasuries is driven by asset‑allocation and risk—rather than politics, although it does have the upside of reducing US dependence.

- Concerns over Fed independence and a diminished commitment to controlling inflation are making Treasuries appear riskier.

Use of Reserves as Strategic Tools

- Gold used to be attractive during low interest rates; gold hedges against inflation, currency debasement, financial market volatility, and geopolitical shock.

- The US and allies froze Russian FX reserves after Russia invaded Ukraine. That revealed that dollar reserves can be used politically by US hostile countries that held dollar reserves.

- Gold is now being bought regardless of real rates because it is viewed as “unsanctionable”.

Why USD Remains the Global Reserve Currency

- There are no competitors on scale or safety, euro is a patch work of sovereign bonds with no US Treasury equivalent, yen and Swiss franc too small, RMB system closed and risky (capital controls and political risk).

- Switching costs very high: funding, derivatives, trade, payments all run on USD.

Conclusion

- Gold demand is rising as a deliberate reserve diversification strategy.

- Political interference with the Fed, rising debt, and fiscal drift erode the dollar’s “safe‑haven” status.

- If global demand for Treasuries falls, expect higher global borrowing costs, and greater volatility.

- Asset class expectations: higher yields and inflation uncertainty pressure equity assets, and gold benefits.

Politicisation of trade and “the rupture of the world order”

Trade is increasingly a key policy variable, with tariffs, sanctions, and trade agreements capable of quickly repricing sectors, regions, and currencies.

“It seems that every day we’re reminded that we live in an era of great power rivalry — that the rules-based order is fading, that the strong can do what they can, and the weak must suffer what they must.”

Mark Carney, Prime Minister of Canada,

Speaking last month at the World Economic Forum, Davos, Switzerland

Transition

- The international system is undergoing a period of transition, as long‑standing global frameworks come under strain. Regional and bloc‑based arrangements are increasingly shaping economic and trade relationships.

- Countries and firms that build diversified market access, multiple, resilient supply routes and credible alliances will be better placed. Those locked into single‑market dependence or politically exposed corridors will face higher volatility in both volumes and pricing.

- Middle countries moving away from the US and China, may face retaliation risk, higher financing costs, and supply‑chain disruption, which can raise inflation and currency volatility. Markets may penalise firms tied to these economies until new trade and finance channels are fully established.

- Winners are likely in logistics & transport, energy infrastructure, flexible industrials, defence/security, and cloud/technology. Losers are those reliant on single markets or politically exposed corridors, e.g. commodities exporters with limited markets, region‑focused consumer firms and companies heavily dependent on large politically exposed infrastructure.

Primer: Gold and silver

There have been significant purchases of gold by sovereign institutions over 2025

Poland: ~102 tonnes

Kazakhstan: ~57 tonnes

Brazil: 43 tonnes

Turkey: ~27 tonnes

China: 27 tonnes

Economic fundamentals between Gold and Silver

Higher Gold prices traditionally reflect global concerns of fiscal stability. Silver tends to follow and amplify the volatility.

Silver has over the last quarter experienced a significant upward spike in prices not seen since the early 1980’s. Nevertheless the ratio of prices between Gold and Silver is close to longer term averages. The questions investors will have is, will precious metals start to exhibit a long‑term upward trend like Bitcoin with prices inflated by limited supply? The first point is to understand the differences between Gold and Silver.

Gold is more likely to experience sustained price escalation if supply growth continues to slow over the next two decades. Silver, by contrast, remains a “flow” metal with regular mining and annual loss. A key point was that Silver was effectively demonetised between 1871 and 1900, when major economies abandoned bimetallism in favour of the gold standard. This shift removed silver from sovereign reserves and permanently broke the historical gold–silver price linkage. Although silver is currently exhibiting elevated volatility, there is little indication that sovereigns will re‑adopt it as a reserve asset in the near term. Consumers, however, may follow a different path. Over the next five to ten years, digital payment systems backed by metal reserves could reintroduce both silver and gold into circulation as point‑of‑sale payment means, representing a potential remonetisation of precious metals outside the sovereign framework.

Market assumption approach

Approach

Approach

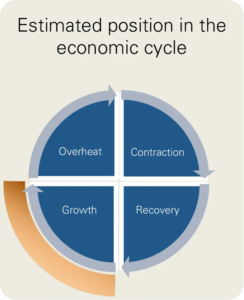

The principle is to consider typical eight‑year returns based on where we are in the economic cycle.

A classical view of the economic cycle is that the economy moves through four stages, growth; economic overheat, requiring intervention from central banks to temper inflation; contraction requiring economic stimulus to get the economy back on its feet; and then recovery as stimulus is scaled back. In real‑life the economy can move backwards or skip a stage compared to this simplified representation.

Market returns can also be impacted by events that fall outside of this cyclical macro‑economic behaviour. Covid‑19 was one such example which led to the global economy cycling very quickly through contraction and back into overheat.

Whilst stock market crashes are possible at all stages of the economic cycle, they are more likely to be deeper and felt wider across the economy when the cycle moves from overheat into contraction.

Position in the economic cycle

While imagination of a new world order is increasingly discussed, global markets remain anchored by US data and policy. Growth remains positive, though muted. Inflation has dropped in the major economies, with unemployment sticky. Sentiment is mixed, with concerns around fiscal policy, but on balance, optimistic. Inflation risks and heightened uncertainty around future Fed independence, on top of those from tariffs, fiscal deficits and the threat of another US government shutdown keep central banks alert and cautious. Current conditions are consistent with mid-cycle in the growth stage, and we have weighted our analysis as 100% growth.

Estimating returns

The return for cash is the SONIA overnight rate for cash expressed as an annualised return.

For assets in the Fixed Income asset classes, we used the latest eight‑year yield to maturity as the annualised return for each of the sub‑asset classes. This is to avoid any arbitrage opportunities within the market return estimates.

For Equities and remaining asset classes, our market data from 1971 is partitioned into four economic stages ‑ Growth, Overheat, Contraction and Recovery. Then we have calculated annualised risk and return for each index over rolling two‑year and eight‑year periods. The analysis is conducted net of UK inflation. We have then added back in current expectations of eight‑year UK inflation to give a return expectation based on current inflation expectations and a probabilistic weighting of where we are in the economic cycle.

Manual adjustments to reflect efficient market pricing

Some risky asset classes do not fit on a neat risk return spectrum, such as the FTSE All‑Share AIM historical risk, and Emerging Market historical returns. For example, FTSE AIM exhibits moderate volatility and very poor historical downside events. Conversely, Emerging Markets has high volatility but low historical returns. For parity, we adjusted FTSE AIM risk upwards in line with observed downside performance. The Emerging Market equity returns were adjusted upwards to be in line with a capital asset pricing model (CAPM), in essence this means that an investor would expect to be compensated with more return for taking on more risk in Emerging Market equities.

Asset class assumptions

Notes on returns and risks given in the table below

Calculation date: 20th January 2026

Assumptions: Nominal returns and risks

Risk horizon: 2 years

Return horizon: 8 years

Yield: Prevailing market rates as at calculation date

Inflation basis: UK market rates from the Bank of England at calculation date

Cycle basis: 100% Growth

Further information

For further information on this document please contact

Managing Director

Dorey Financial Modelling

Office 1, Floor 4

2 Cornet Street

St Peter Port

Guernsey GY1 1BZ

Email: martyn.dorey@doreyltd.com

Direct: 01481 740560

Office: 01481 729044

Mobile: 07839 700717

Web: www.doreyltd.com

Associate Actuary

Dorey Financial Modelling

Unit 1

The Courtyard

Sturton Street

Cambridge CB1 2SN

Email: Robert.Whitfield@doreyltd.com

Direct:01481 740568

Office: 01481 729044

Mobile: 07792 851064

Web: www.doreyltd.com

Consultant

Dorey Financial Modelling

Office 1, Floor 4

2 Cornet Street

St Peter Port

Guernsey GY1 1BZ

Email: Bernadette.kerr@doreyltd.com

Office: 01481 729044

Web: www.doreyltd.com

Important notice

This document has been produced by Dorey Limited, trading as Dorey Financial Modelling. Dorey Financial Modelling does not give advice as to the purchase, sale, subscription for or underwriting of investments, or advice as to the exercise of rights conferred by investments. Dorey Financial Modelling does not perform any delegated investment functions across any of its clients.

Dorey Financial Modelling is not authorised and/or regulated in the United Kingdom by the Financial Conduct Authority (“FCA”) under the Financial Services and Markets Act 2000 or in the Island of Guernsey by the Guernsey Financial Services Commission (“GFSC”). Recipients should also note that they will not be able to bring any complaints about Dorey Financial Modelling to the FCA, the Financial Ombudsman Service or the GFSC or claim compensation from the Financial Services Compensation Scheme.

Certain countries and jurisdictions have restrictions imposed by law on the distribution of information, accordingly, the information that may be viewed is not directed at or intended to be acted upon by anyone in any jurisdiction where it would be unlawful to do so or in which Dorey Financial Modelling would be required to be authorised. It is the responsibility of the recipients to acquaint themselves with and to comply with the laws and regulations that apply to them.

No information given in this document constitutes a solicitation, offer or recommendation by anyone in any jurisdiction to provide any investment advice or services. Recipients confirm that they are eligible to view its content. If any Recipient is not eligible, they should not proceed to read this report. The information contained in this report, which does not purport to be comprehensive, has been compiled by Dorey Financial Modelling.

While this information has been compiled in good faith, no representation or warranty, express or implied, is or will be made and no responsibility or liability is or will be accepted by Dorey Financial Modelling, or by any of its respective officers, employees or agents, in relation to the accuracy or completeness of the document or any other written or oral information made available to any interested party, or its advisers and any such liability is expressly disclaimed. In particular, but without prejudice to the generality of the foregoing, no representation or warranty is given as to the achievement or reasonableness of any future projections, estimates or prospects contained in the document or in such other written or oral information.

This document has been compiled and published by Dorey Financial Modelling. To the fullest extent legally permissible, no reproduction, copying, image scanning, storing, recording or (except as required by law) or modifying of the report by any means in any form nor broadcasting or transmission through any medium of any part of the report is permitted without Dorey Financial Modelling’s prior express written consent. All intellectual property rights that belong to Dorey Financial Modelling in respect of the Modelling work supporting this document are reserved.

These Terms are governed by and construed in accordance with the laws of the Island of Guernsey and Dorey Financial Modelling and all recipients hereby submit to the non‑exclusive jurisdiction of the Courts of the Island of Guernsey.

By viewing this document, recipients agree to be bound by the foregoing Terms.